2021 State of Direct-to-Consumer Brands

By Jared Graf & Kaleigh Moore - Semisupervised

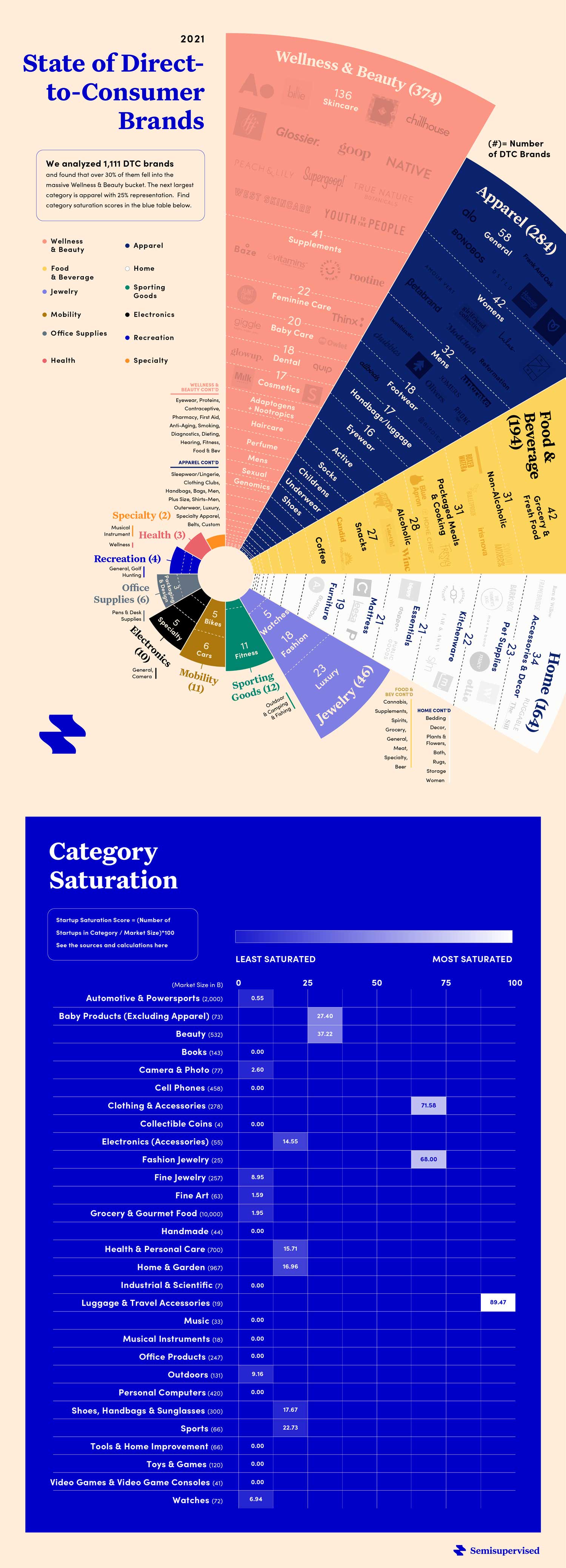

We analyzed 1,111 DTC brands in 2021 to better understand how they fit into the competitive landscape, how saturated their categories are and how much upside remains.

Specifically, we looked at:

• How many DTC brands are in each category• Saturation scores for each category showing you where there's still whitespace

• Trends and changes since last year and the impact on eCommerce from COVID-19

• How to stand out from the crowd in 2021

• And more

Now it’s time to share what we discovered.

Call it DTC’s version of the Cambrian explosion: COVID-19 may have permanently changed the way consumers buy from brands.

eCommerce 3.0 has officially arrived.

It’s been two years since our last State of DTC Brands. Suffice it to say...a lotchanged.

Where has the pandemic left DTC brands in 2021? What does the space look like? And what does that say about how eCommerce 3.0 will unfold?

🕵️♀️ Part 1: Where Do We Stand / Historical Context

Rather than a State of DTC Brands in 2020, we tackled some of the top DTC brands.

In that article, we noticed a few things happening:

• Memberships. In 2020, we saw how memberships with brands helped drive loyalty. And with so many people staying home throughout the year, it’s only helped reinforce the need to get consistent business from the same customers.• Personalization. Our top brand found a way to use machine learning to create personalized skin care solutions for customers. If customers know that they can stick with one brand for a tailored experience, it only drives more loyalty.

A glaring change from 2019-2021: the world has gone remote. Online purchases increased across all business models in 2020 over 2019. eCommerce sales grewover 40%, year-over-year. Toys and games exploded by 135%, while business & industrial brands saw increases of 106%. And those business models include direct-to-consumer brands.

It’s no surprise we’ve seen an explosion in the total number of DTC companies on our list. While the 2019 edition had about 320 brands on the list, 2021 has over 1,100.

However, the increased profitability of online DTC means more competition—and paired with upcoming changes to iOS14, costs to acquire customers will only continue to increase.

“The cost to acquire customers online has gotten prohibitively high,” writes Caroline Jensen of RetailDive. “Direct-to-consumer brands have shoveled millions of dollars into their marketing quarter after quarter.”

Translation: it’s not as simple as opening a DTC brand in a post-COVID world. Some of the best-performing online brands were also brick-and-mortar, according to BlueCore. Those stores now have a key differentiator from online competition: physical space doubles as a billboard.

What does this mean for the current trends in DTC?

To answer that, we have to look at where we were: eCommerce 2.0 and eCommerce 2.5.

• In eCommerce 2.0, platforms like Shopify and BigCommerce provided the platforms. DTC brands could do more than make their own products. They could distribute them from their own online shops.• In what we called eCommerce 2.5, those DTC brands became big names. Handling their own vertical chain—product development, customer feedback, down to fulfillment management—made brands more than just shops. eCommerce 2.0 saw apparel brands emerge, as well. With eCommerce 2.5, Grocery and health shops could now take center stage.

Going into 2019, we saw some trends emerging: Wellness was one of the hottest sub-categories. Opportunities in skincare, vitamins/supplements, genomics, and more were “ripe for innovation,” we wrote at the time.

Last year, our top brands reflected the new reality: grocery and health offerings were here to stay.

Enter eCommerce 3.0.

Here's where we are now — eComm 3.0

So let’s get into eComm 3.0. Here are a few things you’ll notice about today’s top brands:

• Omnichannel is no longer a buzzword. Every DTC interested in scaling is also interested in expanding into brick-and-mortar."I believe that more founders and marketers will understand the need to be everywhere—online and off, retail and wholesale,” said Roger Figueiredo, VP of Marketing at Hashtagpaid. "Being available when consumers want to buy is an underestimated marketing tool. More visibility at points of sale can help challenger brands make inroads against more established competitors."

• Testers come out on top. In a competitive environment, DTCs who know how to run a rigorous testing process across key elements like offers, landing pages, creative and audiences will win precious conversions.

• Retention is more important than ever. That’s especially true with cost-per-acquisition going up amongst online channels. Marketing using personalized communication, such as SMS, saw retention rates as high as 90%.

• Social commerce is reaching the U.S. shores, especially via routes like Popshop Live.

After all, demographics are changing. eCommerce will change with it.

“As Gen Z becomes a primary audience for many, it will be critical to stay on top of trends and emerging technology, while producing content that feels authentic on these new channels,” said Kristen Jones, Director of Marketing at The Groomsman Suit. “Some areas to watch (and get ahead of) will be social commerce, NFTs, and on-site video chat support."

👀 Part 2: Saturation and White Space Opportunities

DTC brands always want to know: where is the daylight? What trends see the most opportunities? Which have low market saturation and high demand? Well, here's a giant graphic that shows exactly that:

Some observations: office products are booming right now. Yet the field had a saturation score of 0, suggesting there’s still plenty of room for growth. That’s despite a huge market size of $247 billion. Plenty of new office gear brands rose through the ranks, highlighting the work-from-home influence of COVID-19.

This highlights a key point in our research. Even though a market can seem saturated due to a large supply of DTC brands, it doesn’t have to indicate a saturated market. The market size may still have room for growth.

"There are still so many opportunities even in categories that feel saturated,” said Nik Sharma of Sharma Brands. “Black Wolf Nation is a great example of a brand that came into a very crowded space but won on price and quality. Now they'll be one of the fastest growing men's skincare brands, and just launched 18 months ago."

Throughout the research, a common theme was how well many brands are defining their niches. Black Wolf is a good example. It targets an underserved audience of men, finding a unique audience in what would otherwise be a highly competitive market. It’s no surprise that other brands are also acquiring brands or creating new DTC brands to capture these niches.

Identifying the right niche also has a positive impact on customer loyalty and retention. For example, one brand with Paris-inspired plus-size clothes saw retention rates of over one-third.

Given how many people stayed home in COVID-19 and stared at their furnishings, it’s no surprise that homeware is an emerging trend. Web traffic for homeware exploded over three times in the last quarter of 2020. Construction costs on new houses and expanded work-from-home opportunities have completely remade an entire industry.

Home and garden brands followed suit. This is another market with such a broad range of appeal that it’s difficult to saturate.

True: the saturation score of 16 does suggest that DTC brands should tighten their focus to specific niches. Large industries like kitchen products, decor, bedding, pool supplies—they all qualify under “home and garden.”

Sustainable fashion was another category with some intriguing upside. Twenty-five of the brands mentioned sustainability. Those included brands in general apparel, handbags, even eyewear. There’s clearly more room in this space.

Grocery and gourmet food also rated well for saturation scores. It’s difficult to saturate a market this large—$12.24 trillion, according to some estimates. More people working and staying home in 2020 helped drive the industry to new highs. That’s despite the presence of new startups looking to meet the demand.

Finally, automotive and power sports did surprisingly well. Shouldn’t people have been doing less driving? Yet each year there are more than 90 million cars sold across the world. And demand is still rising. We saw only 11 startups on the list, suggesting plenty of opportunity for daylight for new DTC brands with big Tiger or Softbank sized coffers.

✨ Part 3: Trends and New Technology

Let's catch you up on some of the most important trends that came out of this year's analysis:

• With the recently rolled out iOS 14.5 changes, first party data is even more critical than ever before. Those with server-side tagging will be at a huge advantage next to those who rely on browser-side.• Buzzwords like “personalization” that have been floating around for years are finally gaining new practical value. Brands are offering more effective quizzes and recommendations for cross-selling. This will be even more important as Big Tech sunsets some of their ad tracking features.

• Whitelisting and user-generated content are no longer niche. In fact, they’ve become the cornerstones of many marketing campaigns. New automated tools like Reeview are emerging in the eComm space, which makes finding and leveraging UGC on product pages easier than ever before.

• Marketplaces and collections of DTC brands. Places like The Fascination and The Quality Edit show just how much consumer interest there is. People want to shop for DTC brands that they feel they’ve “discovered.” And since there's getting to be a critical mass of quality brands, these new DTC marketplaces are growing increasingly important as a result.

• Tools enabling fast checkout workflows are on the rise. “I think these tools are going to continue to rise in importance in addition to the streamlining of online checkouts overall,” said Ian Leslie, CMO of DTC furniture company Industry West. “Whether it's Shop Pay, Bolt’s one-click checkout, or other SaaS tools, the whole checkout ecosystem is evolving rapidly.”

• A huge boom in snacks and beverages. Snaxshot, for example, gained notoriety just for reporting on the emerging trends in the markets. In beverages, we noticed at-home cocktails, tonics, and CBD-infused beverages expanding the width of the market.

• Incumbent brands have been creating their own fresh brands. Co by Colgate, for example, appeals to the image-conscious Gen Z market.

• Amazon and DTC are colliding. But this is a good thing. It offers competition and multiple options for consumers who want more choices. Many consumers turn to DTC for high-value luxury items, as 2pm founder Web Smith noted. “Direct to consumer brands for now are more luxury than they are goods for the everyday human being and I think that’s not going to change anytime soon,” said Smith.

• In previous years, we mentioned skincare as a trend to watch. We’re seeing that come to fruition. Plenty of new skincare brands have hit the market. Many of them are especially focusing on Generation Z, launching on TikTok rather than traditional channels. Brands even held firm in 2020 when there were rumors of a potential ban on TikTok. “These users are not used to being sold to, so when done well, we see conversion rates 3x of Facebook and Instagram,” said Karine Hsu of the design agency Slope.

• Wedding ring DTC brands have illustrated just how vertical the eCommerce 3.0 shop can be. Many are even delivering straight to the consumer’s door.

• Plenty of supplements and vitamin DTC brands are popping up, leading to plenty of competition in an industry worth an estimated $20.7 billion this year.

⛱️ Part 4: Inspiration for the Year

• Creative, creative, creative. Find yourself an effective creative director—or an agency who can outsource the same work. Everyone talks about thumb-stopping creative. But does your creative pass the baby test? The unusual and unexpected get our attention. In the Netflix documentary “Babies,” something unique like an object “defying” gravity earned twice the attention from babies. Adults work the same way. Does your creative garner that kind of attention?• Focus on loyalty. What’s the purpose of creating a DTC brand if you can’t inspire loyalty in those who buy from you? Create clubs, discounts, and memberships to inspire loyalty and reward your existing customers for buying from you. And speaking of that…

• Capture what you have. Conversion rate optimization (CRO) is the way. With online customer acquisition costs going up, it never hurts to cross-sell, up-sell, and retain what you already have. If you haven’t already taken a basic course in CRO, now’s the time.

• FOMO is a major psychological driver. Selling out and back-in-stock notifications are powerful ways to convey value to a world hooked on phone alerts. An example: the “Always Pan” creates exclusivity through limited engagement.

• A humming supply chain is a growth hack. With over 40% YoY growth in eComm last year, 2021 is poised to be another boom year for DTC businesses. Those who can forecast demand, produce and ship more efficiently, will have an advantage in handling this growth. Just ask ShipBob.

• Gen Z is here. We noticed their increasing influence in 2019. Now, while millennials prefer D2C brands by a hair of a margin over traditional retailers, an increasingly-affluent Gen Z prefers online brands at far higher rates. It’s sometimes as high as 45%. That may be one reason that TikTok has such legs in DTC marketing.

• So are the baby boomers. Don’t forget about them! The single fasted-growing market are baby boomers. They have money to spend, and as they grow increasingly tech-savvy, they’ll continue to become an intriguing part of the eCommerce marketplace.

• Tell WILD stories. Ruby and Starface are prime examples: fake backstories that create the sense of an entirely different world. If you’re building a direct brand connection with someone, you might as well take that connection out for a spin. See how far it can go.

• Look for serious differentiation in every stage of the funnel. The more value propositions you can include, the better. The 10 doing well these days include manufacturing, sourcing, certifications, features, benefits, social proof from influencers, and more. Which value propositions are you highlighting at each stage?

• Look for areas of compounding interest. SEO is one example. In the iOS14 world, well-executed SEO is an instant advantage over competition that can stick around for the long-term. And the more content you create, the wider a net you cast.

• In-person stores may not have the traffic they used to, but many people still show loyalty to stores they have nearby and often go online for DTC when they know a brand, which is something DTC startups have to keep in mind.

In summary: The global DTC market is booming. But there's pressure coming from both the top down — with large incumbents finally making meaningful digital investments — as well as the bottom up — with the over half a million new businesses that have started the pandemic.

You won't be to just insert money into Facebook and Google, put them on autobid and expect to win these days. But there's still plenty of upside in the space and it really is early innings. Safe to say it's an exciting time to be in the DTC space, especially if DTC is just one key channel in your omnichannel strategy.

By watching how the audiences change, improving your channel diversity (distribution + marketing channels), honing your testing frameworks, and focusing on first party data, you’ll have much better chance of having a seat at the table for 2021—and beyond.

We hope you found this analysis of the DTC space in 2021 interesting and useful.